Larsen & Toubro (L&T) is one of India’s most prominent engineering, construction, and infrastructure companies. With a strong presence in multiple sectors, including heavy engineering, IT, defence, power, and financial services, L&T is often seen as a proxy for India’s infrastructure and economic growth. In this blog, we’ll explore L&T’s growth drivers, key insights, valuation, and risks to watch.

Stock Overview

| Ticker | LT |

| Industry/Sector | Infrastructure (Construction) |

| Market Cap (Rs Cr.) | 471305 |

| Free Float (% of Market Cap) | 85.4% |

| 52 W High/Low | 3963.5 / 3175.05 |

| P/E | 33.98 (Vs Industry P/E of 28.63) |

| EPS (TTM) | 101.34 |

About L&T

Larsen & Toubro Ltd. (L&T) is a multinational conglomerate headquartered in Mumbai, India. Founded in 1938 by two Danish engineers, Henning Holck-Larsen and Soren Kristian Toubro, the company has evolved into a leading player in engineering, procurement, and construction (EPC), with operations spanning over 30 countries.

L&T operates in key high-impact sectors of the economy, offering end-to-end capabilities from design to delivery.

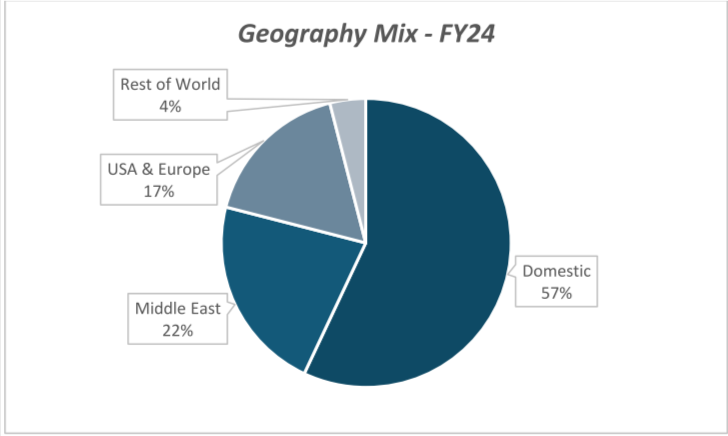

The company caters to government and large corporate clients across various sectors in India and globally. In FY24, 57% of its revenue came from domestic operations, while the remaining 43% was generated internationally.

As of 31st March 2024, the L&T Group comprises 105 subsidiaries, 5 associate companies, 15 joint ventures and 35 jointly held operations.

Key business segments

L&T operates through multiple business verticals:

1. Infrastructure: Engages in large-scale projects, including highways, bridges, metro rail systems, and smart cities.

2. Heavy Engineering: Manufactures critical equipment for nuclear, aerospace, and defence sectors.

3. Power: Specializes in thermal and renewable energy projects.

4. Hydrocarbon Engineering: Covers oil and gas refineries, petrochemical plants, and offshore platforms.

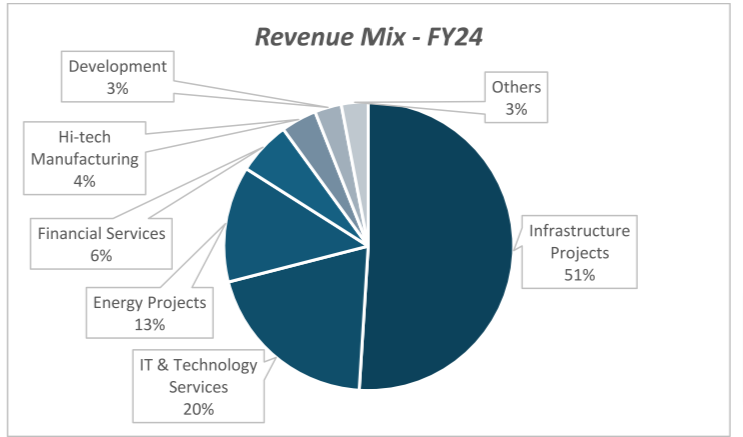

5. IT & Technology Services: Operates through L&T Infotech and Mindtree, focusing on digital transformation.

6. Financial Services: Provides asset management, insurance, and lending solutions.

7. Real Estate & Construction: Develops residential and commercial real estate projects.

Key growth drivers

1. Order pipeline & Execution momentum

L&T anticipates ~10% growth in consolidated order inflows and a 15% increase in revenue for FY25, supported by the execution of its large order book. The order book stands at ₹5,64,223 crore (as of December 31, 2024), with 42% from international markets, ensuring long-term revenue visibility.

2. Government capex & Policy support

The Union Budget 2025-26 has allocated ₹11.21 lakh crore for capital expenditure, which is a 0.9% increase from the previous fiscal year, aiming to stimulate infrastructure growth. Key initiatives like the Bharatmala Project (~₹6.3 Lakh Cr), Smart Cities Mission (~₹2.05 Lakh Crore), and Housing for All will further boost demand in construction, engineering, and urban infrastructure. Additionally, the government’s move to offer ₹1.5 lakh crore interest-free loans to states and its 100% FDI policy in infrastructure are designed to accelerate sectoral growth and remove bottlenecks.

3. Sectoral & Geographical diversification

L&T’s diversified order book comprises 64% infrastructure, 26% energy, and 7% hi-tech manufacturing, reducing dependency on any single sector. The domestic order book consists of 15% from the central government, 26% from the state government, 39% from public sector corporations (state-owned enterprises), and 20% from the private sector. Its international presence (42% of total orders), mainly in the Middle East (92%), benefits from rising investments in oil & gas, industrialization, and energy transition projects.

4. Expansion into high-growth, new-age businesses

L&T is expanding into green energy, semiconductor chip design, digital platforms, and data centers. It has secured 63 MW under the PLI scheme for electrolyzer manufacturing and launched L&T Semiconductor Technologies Ltd., acquiring SiliConch Systems to strengthen its semiconductor capabilities. The company also plans to build ~60 MW of data center capacity, capitalizing on India’s digital infrastructure boom.

Competitor Analysis for L&T

Key Financial Metrics – FY 24;

| Company | Revenue (Rs Cr.) | EBITDA (Rs Cr.) | EBITDA Margin (%) | PAT (Rs Cr.) | PAT Margin (%) | P/E (TTM) |

| L&T | 221112.9 | 29208.5 | 13.21% | 15569.7 | 7.04% | 33.98 |

| IRB Infrastructure | 7409 | 3331.7 | 44.97% | 920.6 | 12.43% | 5.08 |

| Kalpataru Projects | 19626 | 1628 | 8.30% | 516 | 2.63% | 33.21 |

| Afcons Infrastructure | 12637 | 1333 | 11.00% | 411 | 3.25% | 34.99 |

| NCC Ltd. | 20844.9 | 1768.8 | 8.49% | 735.1 | 3.53% | 17.58 |

Key insights on L&T

• L&T has maintained a 10-12% CAGR in revenue over the past five years.

• The company enjoys steady operating margins of 12-15%, with improved efficiencies across projects.

• Its order book remains strong, typically exceeding ₹3 lakh crore, ensuring future revenue visibility.

• L&T has a disciplined capital allocation strategy, divesting non-core businesses while maintaining a stable debt-equity ratio (~1.2x), ensuring financial stability.

• The company consistently pays dividends, maintaining a solid dividend payout ratio of ~34.6%, reflecting its commitment to rewarding shareholders.

Recent Financial Performance (Q3 FY25)

| Metric | Q3 FY24 | Q2 FY25 | Q3 FY25 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (Rs Cr.) | 55127.82 | 61554.58 | 64667.78 | 5.1% | 17.3% |

| EBITDA (Rs Cr.) | 7198.65 | 7917.05 | 7898.16 | -0. 2% | 9.7% |

| EBITDA Margin (%) | 13.06% | 12.86% | 12.21% | -65 bps | -85 bps |

| Net Profit (Rs Cr.) | 2947.36 | 3395.29 | 3358.84 | -1.1% | 14.0% |

| Net Profit Margin (%) | 5.35% | 5.52% | 5.19% | -33 bps | -16 bps |

| Adjusted EPS (Rs) | 21.44 | 24.69 | 24.43 | -1.1% | 13.9% |

L&T reported double-digit growth in Q3FY25, driven by strong performance in the infrastructure and energy segments. Despite steady margins in the core infrastructure business, overall margins declined due to pressure in the energy, IT services (impacted by salary hikes and forex losses), and financial services divisions.

The company recorded a 53% YoY rise in order inflows to ₹1,16,036 crore. Strong execution and a robust order pipeline are expected to help L&T exceed its FY25 revenue and order inflow guidance, supported by domestic capex rebound and international opportunities.

Valuation insights

Larsen & Toubro (L&T) is currently trading at a TTM P/E multiple of 33.98x, reflecting its premium valuation due to its strong order book and execution capabilities. Despite its marginal 1.2% stock price increase over the past year, the company has underperformed the Nifty 50 (8.8%), mainly due to subdued domestic capex and a slowdown in government spending.

However, a healthy order pipeline, both domestically and internationally, coupled with a likely pick-up in execution over the next two quarters, supports revenue growth prospects.

With lifetime-high order book levels, L&T offers strong revenue visibility for the next two years. As infrastructure spending gains momentum, the company is well-positioned to capitalise on these opportunities. Sum-of-the-Parts (SOTP) valuation indicates a potential upside to ₹4,300 levels, suggesting room for further stock appreciation.

Key risks to watch

• Slowdown in Order Inflows: Lower-than-expected order wins, especially in infrastructure and EPC projects, could impact future revenue visibility and growth.

• Lesser than Expected Improvement in Margins: Delays in operational efficiencies, cost overruns, or pricing pressures could result in weaker-than-anticipated margin expansion.

• Rising Input Costs: Fluctuations in raw material prices (steel, cement) and labour costs could put pressure on margins if costs are not effectively passed on.

• Geopolitical & Global Economic Uncertainty: Overseas projects are exposed to economic downturns, forex risks, and geopolitical instability, which may impact international revenues.

Technical Outlook on L&T share price

The stock recently rebounded from the 3270 level, a long-term support zone, and formed a white Marubozu candle, reflecting a bullish sentiment with a price increase of 4.56%. A break above the 3450 level could lead to further upside, with major resistances at 3740 and 3850. If the price sustains above 3600, it may extend its move towards 3800-3900. Currently, the price is trading below its moving averages.

• RSI: 40.98 (Range Bound)

• ADX: 22.63 (Range Bound)

• Resistance: 3660

• Support: 3270

L&T Stock Recommendation

Current Stance: Buy with a target price of ₹4,300 (12-month horizon) and a shorter-term target of ₹3,900.

Why to Buy Now?

L&T’s strong order book, improving execution pace, and favourable domestic & international order prospects provide strong revenue visibility for the next two years. With a pick-up in infrastructure spending and capex recovery, the company is well-positioned for earnings growth. Additionally, its diversified business model, leadership in EPC & construction, and global expansion make it a solid bet for long-term value creation.

Portfolio Fit

L&T is an ideal investment for long-term, growth-oriented investors seeking exposure to India’s infrastructure expansion and global engineering projects. Given its robust execution capabilities, government policy tailwinds, and presence across critical sectors, the stock fits well into portfolios focusing on core industrials, construction, and capex-driven themes.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebL&T: Budget 2025 – 26 Opportunities

• Increased Capex Allocation: ₹11.21 lakh crore for capital expenditure will boost infrastructure projects, providing L&T with significant opportunities in construction and engineering.

• Key Infrastructure Initiatives: Initiatives like Bharatmala (₹6.3 lakh crore) and Smart Cities (₹2.05 lakh crore) present growth prospects for L&T in road and urban development.

• Interest-Free Financing to States: ₹1.5 lakh crore in interest-free loans to states could lead to more state-funded infrastructure projects, benefiting L&T.

• FDI in Infrastructure: The 100% FDI policy will attract more investments in infrastructure, creating more opportunities for L&T’s services in the sector.

• Focus on Renewable Energy: The budget includes allocations for the renewable energy sector, which could open opportunities for L&T in solar, wind, and green infrastructure projects.