In the rapidly evolving landscape of defense and aerospace, few companies have made as significant an impact as Hindustan Aeronautics Ltd. (HAL). A company synonymous with India’s self-reliance in military aviation, HAL is at the forefront of innovation and indigenous defense production.

As India ramps up defense spending and prioritises ‘Make in India’ initiatives, HAL’s strategic positioning in this ecosystem makes it a compelling stock to analyse.

Let’s dive into the fundamentals of HAL, its business segments, growth drivers, key insights, valuation, and potential risks.

Stock overview

| Ticker | HAL |

| Industry/Sector | Capital Goods (Defence) |

| Market Cap (₹ Cr.) | 2,88,576 |

| Free Float (% of Market Cap) | 28.33% |

| 52 W High/Low | 5674.75 / 3046.05 |

| P/E | 32.57 (Vs Industry P/E of 41.54) |

| EPS (TTM) | 130.03 |

About Hindustan Aeronautics Ltd.

HAL, established in 1940, is one of the oldest and largest aerospace and defense manufacturers in the world. It plays a pivotal role in India’s defense infrastructure, producing aircraft, helicopters, avionics, engines, and aerospace components for the Indian Armed Forces and export markets.

Key business segments

Hindustan Aeronautics Ltd. operates primarily in the following key business segments:

- Aircraft manufacturing & upgrades: Builds Tejas fighters, HTT-40 trainers, and transport aircraft while modernising IAF fleets.

- Helicopter division: Produces Dhruv (ALH), Rudra, and LCH for military, paramilitary, and potential civil use.

- Engines & systems integration: Manufactures, overhauls, and services aircraft engines, collaborating globally to boost indigenous tech.

- Defense avionics & accessories: Develops flight control, radar, and avionics systems in partnership with DRDO and global defense firms.

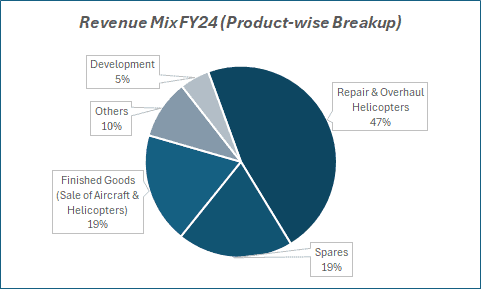

- Exports & MRO: Expanding international presence with aircraft exports and long-term revenue from MRO services.

Primary growth factors for Hindustan Aeronautics Ltd.

Hindustan Aeronautics Ltd.’s key growth drivers:

- Indigenisation & ‘Atmanirbhar Bharat’ – Govt push for domestic defense manufacturing boosts HAL’s revenue via Tejas Mk1A and other contracts.

- Rising Defense Spending – Increasing budgets secure long-term revenue; major orders include Tejas, LUH, and LCH.

- Exports & Collaborations – Expanding global footprint with Tejas, Dhruv, and LCH; partnerships with Safran, Rolls-Royce, and Boeing enhance expertise.

- MRO & Aftermarket Growth – Growing fleet drives MRO demand; HAL expanding support for global clients.

- R&D & Innovation – Focus on AMCA, indigenous engines, and radar systems to reduce foreign reliance.

Detailed competition analysis for Hindustan Aeronautics Ltd.

Key financial metrics – FY 24;

| Company | Revenue(₹ Cr.) | EBITDA Margin (%) | PAT Margin (%) | ROE % | ROCE % | Order Book as of 31st Dec ‘24 (₹ Cr.) | P/E (TTM) |

| Hindustan Aeronautics | 30381.08 | 32.06% | 25.00% | 28.92% | 38.89% | 130000 | 32.57 |

| Bharat Electronics | 20268.24 | 24.90% | 19.45% | 26.12% | 34.97% | 71100 | 41.35 |

| Bharat Dynamics | 2369.28 | 22.65% | 25.86% | 17.99% | 24.39% | 18852 | 83.60 |

| Zen Technologies | 439.85 | 41.10% | 29.44% | 34.13% | 48.86% | 817 | 61.26 |

| Data Patterns Ltd. | 519.80 | 42.64% | 34.95% | 14.59% | 20.19% | 1094 | 53.90 |

Key insights on Hindustan Aeronautics Ltd.

- Achieved a steady revenue CAGR of 9% over 5 years and 10% over 3 years, backed by strong order inflows and execution capabilities.

- Maintains robust EBITDA margins consistently above 30%, reflecting operational efficiency and cost control.

- Delivered impressive profit growth of 26.5% CAGR over the last 5 years, driven by a healthy mix of manufacturing, MRO, and exports.

- Demonstrates a strong return on equity (ROE) track record with a 3-year average ROE of 28.4%, indicating efficient capital utilization.

- Maintains a healthy dividend payout ratio of 29.6%, showcasing commitment to shareholder returns and strong cash generation.

- Working capital cycle has improved significantly, with days reducing from 62.2 to 37.1, reflecting better operational efficiency.

- Strong order book exceeding ₹90,000 crore (~4x annual revenue), ensuring robust revenue visibility for the medium to long term.

- Debt-free with a solid balance sheet, providing financial stability and ample room for future investments and R&D.

Recent financial performance of Hindustan Aeronautics Ltd. for Q3 FY25

| Metric | Q3 FY24 | Q2 FY25 | Q3 FY25 | QoQ Growth (%) | YoY Growth (%) |

| Revenue (₹ Cr.) | 6061.28 | 5976.29 | 6957.31 | 16.42% | 14.78% |

| EBITDA (₹ Cr.) | 1435.33 | 1639.96 | 1682.51 | 2.59% | 17.22% |

| EBITDA Margin (%) | 23.68% | 27.44% | 24.18% | -326 bps | 50 bps |

| PAT (₹. Cr.) | 1254.86 | 1498.46 | 1434.36 | -4.28% | 14.30% |

| PAT Margin (%) | 20.70% | 25.07% | 20.62% | -445 bps | -8 bps |

| Adjusted EPS (₹) | 18.86 | 22.59 | 21.53 | -4.69% | 14.16% |

Hindustan Aeronautics Ltd. financial update (Q3 FY25)

Financial performance:

- Revenue from Operations: Increased by 15% year-on-year (YoY) to ₹6,957 crore.

- Net Profit: Rose by 14% YoY to ₹1,434 crore, driven by sustained demand from the Indian defence ministry.

- Dividend declaration: Declared an interim dividend of ₹25 per share for fiscal 2025.

Operational highlights:

- Order acquisition: Secured a significant order worth ₹13,500 crore in December 2024 for 12 Sukhoi fighter jets from the Indian government.

- Spares and repair business: This segment continues to constitute a substantial portion of HAL’s total sales, contributing to overall revenue growth.

Company valuation insights – Hindustan Aeronautics Ltd.

Hindustan Aeronautics Ltd (HAL) trades at a TTM P/E of 32.57, below the industry average of 41.54, with a 22% 1Y return vs. the Nifty 50’s 3.3%. Its ₹90,000+ crore order book (~4x annual revenue) ensures long-term earnings visibility. HAL benefits from rising defense spending, the ‘Atmanirbhar Bharat’ push, and increasing global demand for Tejas, Dhruv, and LCH.

With EBITDA margins above 30%, 26.5% profit CAGR, and 28.4% ROE, HAL maintains strong financials. A debt-free balance sheet and improved working capital cycle (62.2 days to 37.1 days) further strengthen its position.

A DCF valuation with 12% FCF growth, 11% discount rate, and 5% terminal growth rate gives an intrinsic value of ₹4,390. Factoring in strategic positioning, we set a target price of ₹4,900, implying a 14% upside.

Major risk factors affecting Hindustan Aeronautics Ltd

- Execution Delays: Past delays in Tejas Mk-1A deliveries raise concerns over timely execution and cost overruns.

- Order Flow Uncertainty: Delays in new orders despite AoN approvals may impact revenue visibility.

- Raw Material Cost Pressure: Rising input costs could compress margins in upcoming projects.

- High Government Dependence: Reliance on Indian defense budgets makes HAL vulnerable to procurement delays or budget cuts.

- Rising Competition & Supply Chain Risks: Growing private sector participation and dependence on foreign components pose long-term strategic and operational risks.

Technical analysis of Hindustan Aeronautics Ltd. share

HAL has recently broken out from a descending channel, followed by a strong upward move. The stock is trading above its 50-day and 100-day moving averages and is about to cross its 200-day moving average from below, indicating positive momentum.

The MACD remains firmly positive at 196.49, with the MACD line above the signal line, supporting the continuation of the uptrend. The RSI is at 74.35, reflecting strong buying interest, while the relative RSI for both 21 and 55 days is significantly positive at 0.29 and 0.12, indicating strong outperformance against its benchmark. The ADX at 36.34 suggests a well-established trend.

If the stock sustains above its immediate resistance of ₹4,500, crossing its 200-day moving average from below, it could move towards the target price of ₹4,900. On the downside, strong support is seen at ₹3,950.

- RSI: 74.35 (Overbought)

- ADX: 36.34 (Strong Trend)

- MACD: 196.49 (Positive)

- Resistance: ₹4,500

- Support: ₹3,950

Hindustan Aeronautics Ltd. stock recommendation

Current Stance: Buy with a target price of ₹4,900 (12-month horizon); HAL’s strong order book, improving execution, and robust financials position it well for sustained growth despite execution challenges.

Why buy now?

Government Support: ‘Atmanirbhar Bharat’ and rising defense budgets provide long-term revenue visibility.

Order Book Strength: ₹90,000+ crore backlog (~4x annual revenue) ensures multi-year earnings growth.

Export Potential: Global interest in Tejas, Dhruv, and LCH could drive new international contracts.

Margin Resilience: EBITDA margins remain above 30%, supported by operational efficiencies.

Debt-Free Growth: Strong balance sheet and improving working capital cycle enhance financial stability.

Portfolio Fit:

HAL is a high-quality, debt-free defense player with strong earnings visibility, high margins, and robust return ratios. It is an ideal choice for investors seeking long-term exposure to India's growing aerospace & defense sector.If you found this helpful and want regular stock trade calls, check out my community on StockGro here: https://app.stockgro.club/ui/social/tradeViews/groupFeed/07a7b961-b8ca-42ce-baf3-a9eec781b6ebHindustan Aeronautics Ltd: Budget 2025-26 opportunities

- Increased Defense Allocation: Higher capital outlay for defense in the Union Budget will drive more procurement orders for HAL, strengthening revenue visibility.

- Boost to Indigenization: Government incentives for domestic defense manufacturing under ‘Atmanirbhar Bharat’ will enhance HAL’s long-term growth prospects.

- Export Promotion Initiatives: Policy support for defense exports and easing of approval processes can accelerate HAL’s global market expansion.

- R&D Incentives: Increased allocation for defense R&D will aid HAL’s indigenous development of next-gen fighter jets and engine technology.

- Stronger MRO Push: Budgetary focus on aircraft maintenance, repair, and overhaul (MRO) will create new revenue streams for HAL’s after-market services.

Final thoughts

Hindustan Aeronautics Ltd. is a cornerstone of India’s defense sector, benefiting from strong policy support, a growing defense budget, and increasing export opportunities.

Its robust order book, healthy financials, and strategic positioning make it an attractive long-term investment. While execution risks and government dependence remain concerns, HAL’s leadership in the domestic aerospace industry and its expansion into global markets make it a stock worth considering for investors looking to capitalise on India’s defense modernisation drive.