Stock overview

| Ticker | INDUSINDBK |

| Sector | Banking & Financial Services |

| Market Cap | ₹ 77,100 Cr |

| CMP (Current Market Price) | ₹ 935 |

| 52-Week High/Low | ₹ 1,576/ ₹ 923 |

| P/E Ratio | 10.3 x |

| Beta | 1.2 (Moderate volatility) |

About INDUSIND Bank

IndusInd Bank is the 5th largest private sector bank in India, serving over 40 million customers nationwide. It is also India’s 2nd largest microfinance lender, operating through its subsidiary Bharat Financial Inclusion Limited (BFIL), serving over 13 Mn customers. With the scale and growth outlook, is it a good buy for investors at the current market price ? Let’s find out.

Primary growth factors for INDUSIND Bank

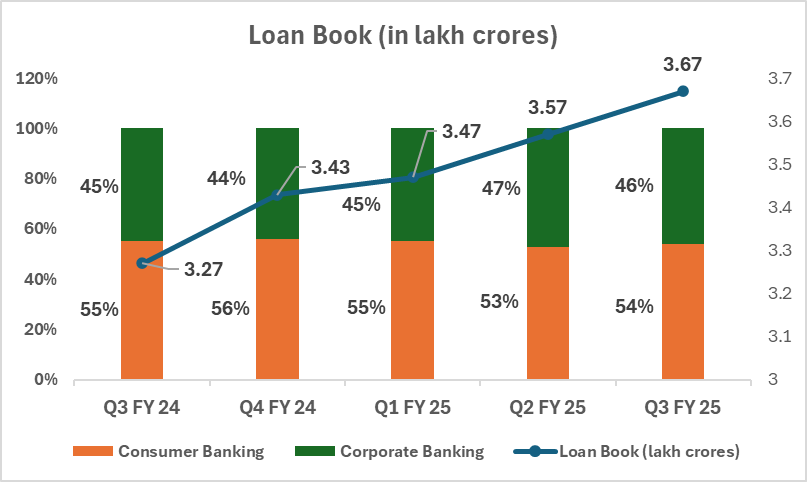

1. Strong loan book & Diversified portfolio

- IndusInd Bank reported a strong loan book growth of 12% on a YoY basis from 3.27 lakh crore to 3.67 lakh crore. They also registered a 3% growth in loan book on a QoQ basis.

- Their loan book is well diversified across consumer banking (55% of loan book) and corporate/commercial banking (45% of loan book).

Here’s the trend of their loan book on a QoQ basis

2. Recent Q3 FY25 Financial Performance

| Metric | Q3 FY 25 | YoY Growth | QoQ Growth |

| Net Interest Income | 5,228 cr | -1% | -2% |

| Operating Profit | 3,601 cr | -11% | 0% |

| Profit before Tax | 1,858 cr | -40% | 4% |

| Profit after Tax | 1,402 cr | -39% | 5% |

- INDUSIND Bank reported flat revenue growth in Q3 FY25.

- The bank saw an 80% surge in the overall provisions and contingencies which put a pressure on their overall profitability.

- Investors should keenly watch out for the bank’s provisions from here on because that will dictate the trend of overall profitability for the bank.

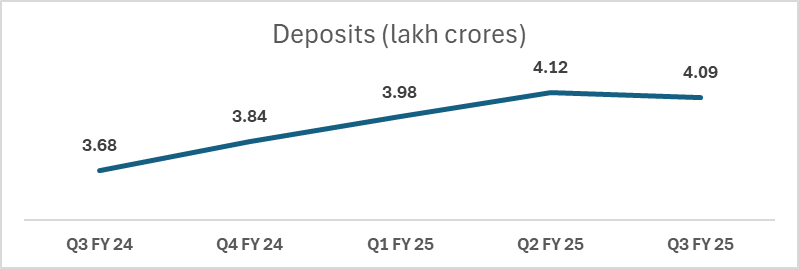

3. Healthy deposits growth

- INDUSIND Bank reported an 11% YoY growth in total deposits.

- The bank also reported a healthy share of CASA of 35% with a 1% YoY Growth in total CASA deposits.

Detailed competition analysis for INDUSIND Bank

| Company | Market Cap | Profit | P/E | RoCE |

| INDUSIND Bank | 77,100 cr | ₹ 1,401 cr | 10.3x | 7.9% |

| HDFC Bank | 13,25,400 cr | ₹ 17,656 cr | 18.8x | 7.7% |

| ICICI Bank | 8,50,500 cr | ₹ 12,880 cr | 17.4x | 7.6% |

| Kotak Bank | 3,78,300 cr | ₹ 4,700 cr | 19.3x | 7.9% |

- The stock is relatively undervalued compared to its peers with a P/E of 10.3x and a PBV of 1.2x.

Company valuation insights : INDUSIND Bank

As per Discounted Cash Flow analysis:

It estimates the intrinsic value of IndusInd Bank share based on expected future cash flows:

- Intrinsic Value Estimate: ₹1,090 per share

- Upside Potential: 15%

- WACC: 11%

- Terminal Growth Rate: 5%

Major risk factors affecting INDUSIND Bank

- Economic slowdown: A weaker economy may affect credit demand and increase defaults.

- Asset quality concerns: Any sharp rise in NPAs could pressure profitability.

- Regulatory changes: New banking regulations or tighter norms may impact operations.

- High competition: Intense competition from larger peers could limit market share growth.

- Interest rate sensitivity: Fluctuating interest rates may affect NIMs and overall profitability.

Technical analysis of INDUSIND bank

- Current trend: The stock has sharply corrected from 1400 odd levels and is currently trending in the range of 950-975. Further an overall correction in the stock market has also inflicted pain for the investors of this stock.

- Support level: ₹925

- Resistance level: ₹1,1050

INDUSIND stock recommendation by Ketan Mittal

Current Stance: BUY with a 12-month target of ₹1,090.

Rationale:

Consistent loan growth with a diversified loan book.

Strong capital adequacy and deposit growth.

Undervalued stock relative to sector peers.If you found this helpful and want regular stock trade calls, check out my StockGro profile here: https://stockgro.onelink.me/vNON/6m6ykj0dConclusion

IndusInd Bank’s solid fundamentals, resilient business model, and discounted valuation make it a compelling long-term investment. The bank is well-positioned to benefit from India’s economic growth, digital banking adoption, and declining credit risks, presenting an attractive risk-reward opportunity for investors.