On Tuesday, April 23, Tata Consumer Products Ltd (TCPL) announced that its net profit declined by 19% year-on-year (YoY) to ₹217 crore for the period ended March 31, 2024.

Tata Consumer Products Q4 results for the financial year 2024 were a mixed bag – while revenue grew, profit fell short of expectations. This suggests the company sold more but did not make as much money on those additional sales as analysts had predicted.

Want to know more about how the company performed in Q4FY24 and did it beat the estimates? Let’s find out!

About Tata Consumer Products

Tata Consumer Products Limited (TCPL), a subsidiary of the Tata Group, is a major player in India’s Fast Moving Consumer Goods (FMCG) sector. The company was formed as a result of a merger between Tata Global Beverages Limited (TGBL) and Tata Chemicals Limited (TCL).

Previously known as TGBL, it has rebranded itself to be called Tata Consumer Products, and it includes popular brands such as Tetley, Tata Tea, Eight O’Clock Coffee, Tata Salt, and Himalayan Water. It also has brands like Tata Sampann, Tata Gluco Plus, Tata Soulfull, and Tata Water Plus.

Besides being the world’s second-largest branded tea player and significant coffee producer; it is also the biggest salt brand in India. The company’s registered office is situated in Kolkata, India, while its corporate headquarters can be found in Mumbai.

Its presence that covers North America, Canada, Europe, Australia, the UK, Middle East among others allows it to reach out to more than 263 million Indian homes while its products are delivered through four million retail outlets worldwide. This organisation aims to become a top diversified consumer products firm.

The shareholding pattern of the company as of 31st March 2024 is:

| Investor Type | Percentage Held |

| Promoter and Promoter Group | 34% |

| Individual Investors | 19% |

| Mutual Funds/UTIs/AIFs | 7% |

| Insurance Companies/Banks | 10% |

| Foreign Institutional Investors | 25% |

| Others | 5% |

Quarterly performance

Tata Consumer results – Q4

On April 23, 2024, Tata Consumer Products announced a consolidated net profit of ₹217 crore for Q4FY24 ending March 31. This represents a 19.3% decrease from the ₹269 crore reported during Q4FY23.

The company’s consolidated revenue from operations for Q4FY24 was ₹3,927 crore, marking an 8.5% increase compared to ₹3,619 crore during the same period last year.

The Consolidated Earnings Before Interest, Taxes, Depreciation, and Amortisation, commonly referred to as EBITDA, for the quarter was ₹631 crore, a 22% increase. The EBITDA for the entire year (FY24) rose by 24% to ₹2,323 crore.

Tata Consumer Products reported a 7.4% rise in total expenses at ₹3,456 crore year-on-year (Y-o-Y), up from ₹3,217 crore.

For the full financial year of FY24, the company reported a net profit of ₹1,150 crore, a 4.4% decrease compared to ₹1,203 crore at the end of FY23.

The total revenue for FY24 increased by 10.3% to ₹15,206 crore, compared to ₹13,783 crore reported at the end of the previous year. Total expenses at the end of FY24 increased by 9% to ₹13,429 crore Y-o-Y, up from ₹12,318 crore.

QoQ performance

| Period | Q4FY24 | Q3FY24 | Q-o-Q Growth | Q4FY23 | Y-o-Y Growth |

| Total Revenue (₹ crore) | 3926.94 | 3803.92 | +3.23% | 3618.73 | +8.52% |

| Total Operating Expense (₹ crore) | 3575.9 | 3408.58 | +4.91% | 3204.03 | +11.61% |

| Operating Income (₹ crore) | 351.04 | 395.34 | -11.21% | 414.7 | -15.35% |

| Net Income (₹ crore) | 216.63 | 278.9 | -22.33% | 268.59 | -19.35% |

Tata Consumer Products Q4 results – Expectations vs reality

Analysts expected that Tata Consumer Products are poised to outperform the downturn in the consumer sector. This is due to its industry-leading revenue growth in the mid-single digits and a strong margin expansion that has led to even faster profit growth.

Analysts predicted that the company’s revenue growth will top its industry peers, thanks to increased sales of beverages, a rise in salt volumes, and the acquisition of Capital Foods, the company behind the Ching’s Secret brand.

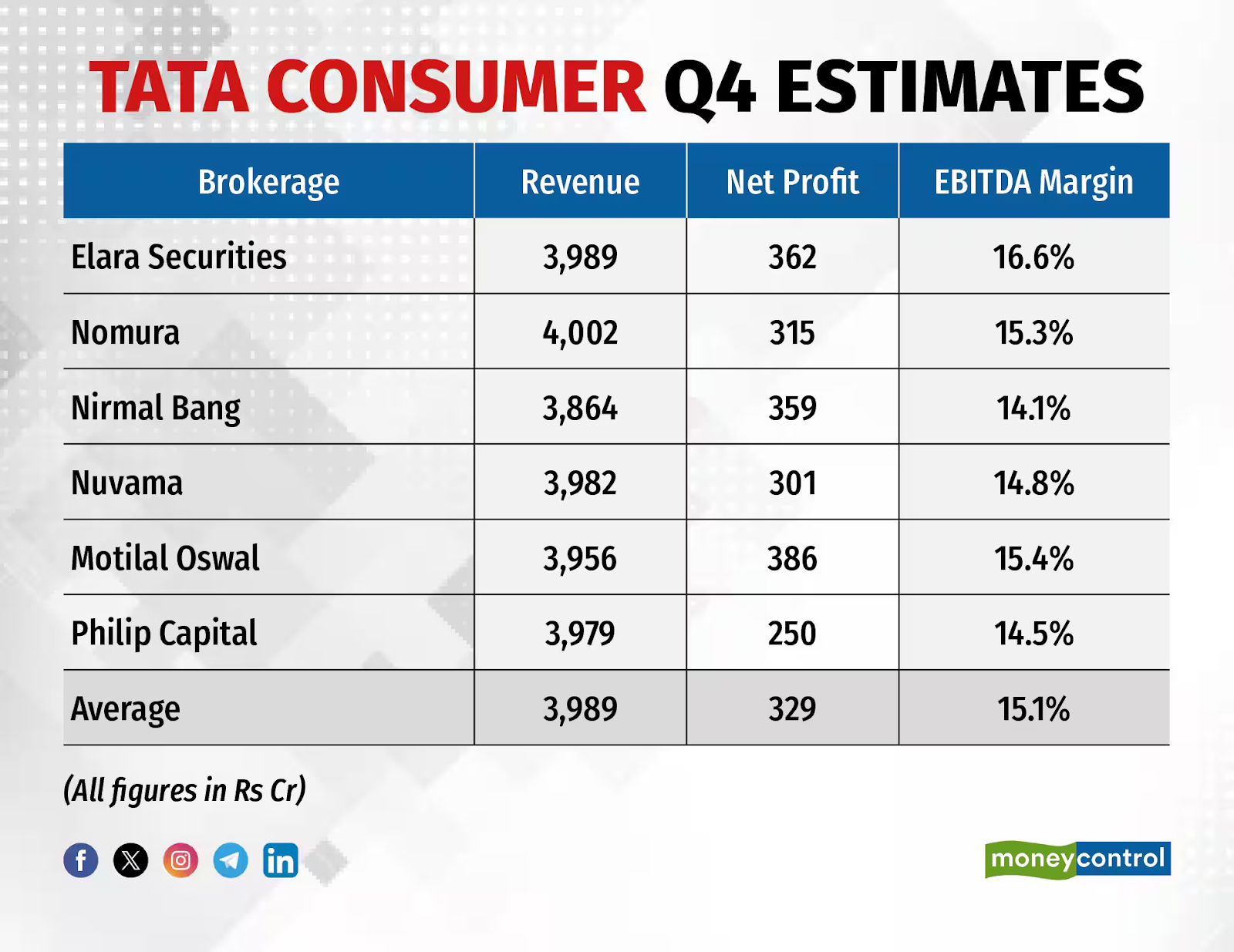

While the revenue was largely as expected, the profit fell short of estimates. A poll of six brokerages by Moneycontrol had projected a year-on-year revenue growth of 4.8% to ₹ 3,989 crore. The net income was expected to increase by 13.4% to ₹329 crore.

Tata Consumer reported an EBITDA margin of 16%, which was 90 basis points higher than the EBITDA margin of 15.1% predicted by a Moneycontrol poll.

Let’s see how Tata Consumer Products performed in comparison to estimates based on Moneycontrol poll:

| Analysts’ Predictions | Actual Figures | Expectations (Above/Below) | |

| Revenue (₹ crore) | 3989 | 3926.94 | In line |

| Net Profit (₹ crore) | 329 | 216.63 | Below |

| EBITDA Margin (%) | 15.1 | 16 | Above |

Tata Consumer Products’ competitors

Here are some of the market competitors of Tata Consumer share, ranked by their market capitalisation as of 25th April 2024:

- CCL Products India – ₹7754.68 crores

- Vintage Coffee & Beverages Ltd – ₹663.39 crores

- Goodricke Group Ltd – ₹368.05 crores

Stock price

If we look at the Tata Consumer share price history, it has given a return of 418.22% in the past five years and a return of 47.96% in the past one year (as of 25th April 2024).

Let’s talk about the Tata Consumer Products share target (as of 24th April 2024). Various research agencies have provided the following price targets:

- Morgan Stanley – the target of ₹1,305 per share

- Nuvama Institutional Equities – ₹1,400 per share

- CLSA – ₹1,288 apiece

- ICICI Securities – ₹1,360

Bottomline

Tata Consumer Products Ltd (TCPL) had a mixed Q4FY24. However, it remains strong in the competitive FMCG space with well-known brands and wide market reach. Its future performance is key to achieving its vision of being one of the best-diversified consumer goods companies.

The stock has given significant returns over the years, and many research agencies have set bullish price targets for it. The company’s strategies and performance in future quarters will be closely monitored by investors and those who keep a close eye on the market.