Table of contents

Imagine you’re on a treasure hunt, but instead of searching for gold, you’re navigating the financial landscape of a company. You’ve found the treasure chest of operating income, but there’s more. Hidden away, often overlooked, is another valuable gem – non-operating income.

This elusive income, not derived from a company’s primary business operations, holds secrets to the company’s overall financial health. It’s like finding a hidden room in a treasure cave. By understanding non-operating income, you, as an investor or stakeholder, can unlock a more comprehensive view of a company’s financial performance.

Ready for the adventure? Let’s dive into the intriguing world of non-operating income, its components, and its significance in financial analysis. The journey promises to be enlightening!

What is non-operating income?

In its simplest form, non-operating income is the money a business makes from doing things unrelated to its main business. This is similar to when a company gets an unexpected benefit that has nothing to do with its main business activities.

For example, if a company that mostly makes cars sells a piece of property it owns, the money it makes from the sale would be considered non-operating income. This is because selling real estate is not the main business of the company; their main business is making cars.

It’s important to understand non-operating income because it can have a big effect on a business’s overall profitability and financial health. However, since it’s not a steady source of income, it’s usually left out of evaluations of a business’s running efficiency.

Components of non-operating income

There are different parts of non-operating income, and each one helps the company’s overall finances uniquely. Here are a few of non-operating income examples:

- Dividend income

- Gains due to investment in financial securities

- Foreign exchange gains

- One-time non-recurring gains

- Recurring but non-operating gains

Case study

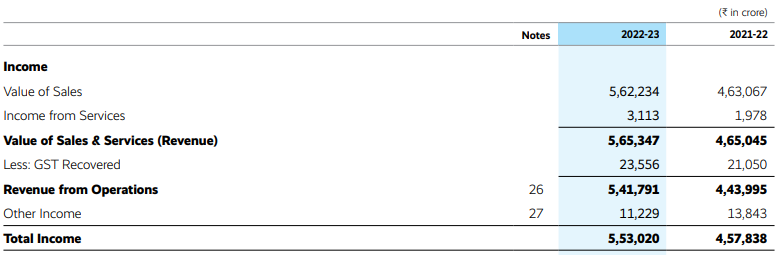

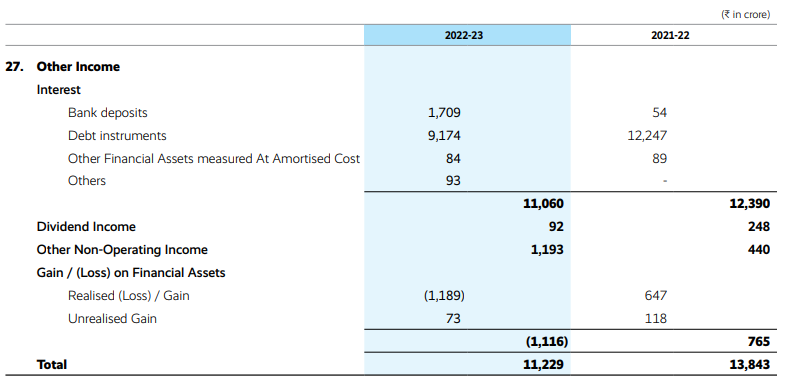

Let’s take a look at a real-life example to understand the concept on a deeper level. These are the extracts of the standalone financial statements of Reliance Industries Ltd.

Extract 1 – Statement of profit and loss – For the year ended 31st March, 2023

Extract 2 – Notes to accounts – Note 27: Other income

The line item for non-operating income follows the operating profit line item at the bottom of the income statement.

Advantages and disadvantages of non-operating income

Even though non-operating income doesn’t come from a company’s main business activities, it can greatly affect its overall financial health. Some pros and cons of non-operating income are listed below:

Advantages:

Diversification: A company can diversify its revenue streams and, in theory, lower its overall risk exposure by generating non-operating income.

Profitability: A company’s bottom line can see a boost from non-operating income, particularly if it’s generated from lucrative investments or substantial asset sales.

Financial analysis: The ability to disentangle the revenue from core operations from peripheral activities is a key component of a thorough financial analysis, and non-operating income provides just that.

Disadvantages:

Volatility: Due to reliance on market factors like investment returns and currency exchange rates, non-operating income can fluctuate wildly.

Tax implications: The tax burden of the business may rise due to non-operating income.

Misrepresentation of performance: The company’s performance is impacted when non-operating income is negative because it lowers the net income. A misrepresentation of the company’s real operational performance might result if it is artificially inflated to offset losses on operations.

Difference between operating income and non-operating income

| Operating income | Non-operating income | |

| Definition | A company’s operational income is the money it makes from running its main business. | Non-operating income refers to a company’s earnings from sources other than its core business activities. |

| Source | Primary sources | Secondary sources |

| Example | Sale of merchandise | Rental earnings |

| Impact | A strong indication of how efficiently and profitably a business runs its operations is its operating income. | It can paint a fuller picture of the state of a business’s finances |

Special consideration

Companies will sometimes use large amounts of non-operating income to artificially inflate their earnings to hide their bad operational performance. EBIT may include income from non-core activities, which could be inflated to hide lacklustre results.

It is critical to be on guard in case management teams try to highlight metrics that include these exaggerated gains. It is critical to determine the source and sustainability of non-operating income since it can artificially enhance earnings.

Regardless, there are benefits to non-operating income. It helps stakeholders evaluate operational performance by providing a metric to measure revenue from non-core activities. Furthermore, stakeholders are more likely to support the company’s growth goals when such income and expenses are openly disclosed.

Bottomline

Even though it is generated from non-core operations, non-operating income can significantly impact a company’s overall profitability and financial health. Therefore, stakeholders must consider both operating and non-operating income when assessing a company’s financial performance.

FAQs

Income from non-operating assets refers to the earnings a company generates from assets that are not involved in its primary business operations. These assets, which can include investments, real estate, or marketable securities, can provide a company with additional revenue streams. While they may not contribute to the company’s core operations, they can significantly impact its overall financial health and profitability.

Non-operating activities refer to those transactions or events that are not related to a company’s primary line of business. These activities can significantly impact a company’s revenues, expenses, or cash flow, but they fall outside the company’s routine, core operations. Examples include gains or losses from investments, foreign exchange, and sale of assets. While they may not contribute to the company’s core operations, non-operating activities can significantly affect its overall financial health.

Yes, income tax is considered a non-operating expense as it is not related to the core business activities. It includes federal, state, and local income tax expenses. However, it’s important to note that not all taxes are non-operating expenses. For instance, payroll, sales, or property taxes, which are related to the operation of the business, are considered operating expenses.

Non-operating liabilities are obligations that are not related to a company’s primary business operations. They might include debts or amounts owed by the company that are unrelated to its normal business affairs. For instance, a mortgage on a property that is not used in the company’s core operations could be considered a non-operating liability. These liabilities are crucial to consider when assessing a company’s overall financial health.

Net profit, also known as net income or net earnings, is a key measure of a company’s profitability. It is calculated by subtracting total expenses from total revenue. The formula is:

Net Profit=Total Revenue−Total Expenses

Total revenue is the total sales minus discounts and refunds, while total expenses include costs of goods sold, administrative costs, taxes, and other operating expenses.