Table of contents

Perpetual bonds are like regular bonds, but without a maturity date.

In the dynamic world of finance and investing, stocks and bonds are the bread and butter. But perpetual bonds are the cheese. Perpetual bonds are gaining more attention from seasoned investors and newcomers alike. There’s a reason why these assets are carving out a place for themselves in the investment landscape.

Perpetual bonds, with no maturity date, are underexplored assets that can diversify your portfolio and potentially beat the market.

This article discusses the meaning of perpetual bonds, their differences from regular bonds, when to consider investing in them, and their suitability for your portfolio. Let’s dive in.

What is bond investing?

To understand perpetual bonds, let’s get into how regular bond investing works. Imagine you have ₹10,000 to invest for one year. You decide to invest in bonds. These could either be government bonds or corporate bonds.

‘Investing in bonds’ means that you’re loaning your capital to a large entity that needs your money for a particular period. This period is the maturity date. At maturity, you get back your principal along with some interest for your risk. So, at a 4% bond yield, your ₹10,000 turns into ₹10,400 over one year. Bonds hence, at the base level, are special promissory notes that list down the above agreements for both parties.

What is a perpetual bond?

In perpetual bonds, you lend ₹10,000 and receive ₹125 annually forever, without the return of the principal amount. That is why it is also called a forever bond.

So, the company that sells you the perpetual bond gives you ₹125 the first year, and then another ₹125, then another, and then another in perpetuity. This goes on as long as you continue to live. Since there’s no specific maturity date, the company doesn’t have to give you the principal back. The only way you get your money back is through these regular payments.

Here’s a difference summary between regular bonds and perpetual investing:

- End date – In a regular bond, there’s a fixed date when you get your money back, but in a perpetual bond, there’s no fixed end date.

- Getting back the principal – In a regular bond, you get back your original ₹10,000 at the end, but in a perpetual bond, you don’t; you keep getting smaller payments (₹125 in the example) indefinitely.

- Risk – Perpetual bonds carry more risk than regular bonds. If the issuer goes bankrupt or insolvent, you may stop receiving payments, even if you haven’t recouped your initial investment.

Are payments truly unending?

This is a valid concern amongst perpetual bond investors. However, these investments do provide an ongoing income stream to their holders in perpetuity.

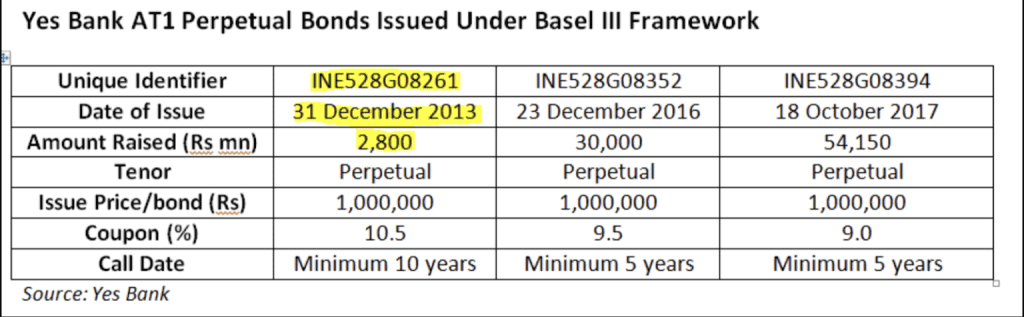

Perpetual debt instruments issuers can choose to redeem these bonds, typically after a set period of 10 years. ‘Calling’ the bond returns the original principal, ending the ‘perpetual’ agreement. This flexibility is beneficial as it allows issuers to decide when to redeem, due to the bonds’ indefinite maturity dates.

The issuer’s ability to determine the timing of redemption may be a primary reason why they opt to issue perpetual bonds in the first place.

Calculating returns from a perpetual bond

Just like any other investment, you need to calculate your cost-benefit ratio when investing in perpetual bonds. The formula goes like this:

Present value of a perpetual bond = D/r

Where D = the regular payment of the bond,

and r = the discount rate applied to the bond.

A bond discount is the difference between the bond’s market price and its maturity value, leading to capital gain at maturity.

Hence, if a bond pays ₹400 in perpetuity to the investor and the discount rate applied is 5%, then the current value of the bond should be:

Present value = ₹400/0.05 = ₹8,000.

The bond’s present value is highly sensitive to the discount rate. As the rate increases, the present value goes down.

Should you invest in perpetual bonds?

Perpetual bonds may not suit everyone’s investment goals and risk tolerance. However, they can be beneficial for certain investors looking to diversify their portfolios.

- Income-oriented investors – Retirees can invest in perpetual bonds for a continuous passive income.

- Long-term investors with high-risk tolerance – Young investors with spare cash and time until retirement can invest a small part of their portfolio in perpetual bonds due to their higher risk tolerance and liquidity.

- Sector-specific investors – Perpetual bonds allow fund managers and high-net-worth investors to diversify, minimize risk, and stay invested in promising sectors while retrieving their initial investment.

- Investors seeking diversification – Perpetual bonds allow investors to diversify their funds across sectors and investment types, providing a hedge against bear markets and crashes.

Tax on Perpetual Bonds

Income from perpetual bonds is added to your annual income and taxed based on your tax slab. However, in other exceptional circumstances where these bonds are sold to other buyers in a secondary market, a capital gains tax worth 10% might also be applicable. We encourage you to consult a tax professional if you’re unsure about your tax liability when investing in perpetual bonds.

Want to test your trading skills without risk? Use StockGro’s virtual trading platform and refine your strategies. Start with virtual trading app now!FAQs

Perpetual bonds, with no maturity date, provide a steady, predictable income. They’re less sensitive to interest rate changes, making them appealing in a low-interest-rate environment. However, they expose investors to the issuer’s credit risk indefinitely. While they offer the potential for higher theoretical returns, they may not yield maximum gains compared to other bonds. Investment suitability depends on individual financial goals and risk tolerance.

Yes, perpetual bonds can be sold. They are traded on stock exchanges, providing investors with flexibility and liquidity. If an investor wishes to liquidate their investment, they can do so by selling the bonds on the stock exchange. This feature gives investors the freedom to manage their holdings according to their financial needs and market conditions.

Perpetual bonds, having no maturity date, do not have a yield to maturity in the traditional sense. However, their value can be calculated using a formula similar to yield to maturity. The price of a perpetual bond is the fixed interest payment, or coupon amount, divided by a constant discount rate, which represents the speed at which money loses value over time.

Yes, perpetual bonds are considered hybrid instruments. They combine the characteristics of both bonds and equities. Like bonds, they pay a fixed coupon, usually semi-annually. However, similar to equities, they have no maturity date. This unique combination allows them to offer a steady income stream like bonds, while also having the potential for long-term returns associated with equities.

Bonds do not lose value after maturity. When a bond reaches its maturity date, the principal amount (also known as face value) is returned to the bondholder. However, if a bond is sold before its maturity date, its market value can fluctuate based on factors like interest rates and the creditworthiness of the issuer. Therefore, holding a bond until maturity ensures the return of the initial investment.